Table of Contents

- 1. Introduction: The Online Shopping Card Dilemma

- 2. The Core Difference in One Sentence

- 3. Reward Structure: HeadtoHead Comparison

- 4. When BOBCARD Cashback Wins

- 5. When Snapdeal BOBCARD Wins

- 6. The July 2025 Snapdeal BOBCARD Change: What Cardholders Need to Know

- 7. Monthly Value Comparison: RealWorld Scenarios

- 8. Annual Fee Analysis: True Cost of Ownership

- 9. Network Comparison: Mastercard vs RuPay

- 10. Customer Experience and Card Management

- 11. Who Should Apply for Which Card?

- 12. The Verdict

- 13. Frequently Asked Questions

Key Takeaways

- BOBCARD Cashback (₹499/year) gives 5% on ALL eligible online platforms - Amazon, Flipkart, Myntra, and more - with a monthly cap of ₹1,500.

- Snapdeal BOBCARD (₹249/year) offers unlimited 5% cashback specifically on Snapdeal - no monthly cap on Snapdeal purchases.

- BOBCARD Cashback autocredits cashback monthly with zero effort; Snapdeal BOBCARD requires manual redemption (from July 2025).

- The Snapdeal BOBCARD uses the RuPay network and supports UPI payments, while BOBCARD Cashback runs on Mastercard with no UPI linking.

- Both cards lack travel perks, lounge access, or dining benefits - they are pure online shopping cards.

- For heavy multiplatform shoppers, BOBCARD Cashback wins; for dedicated Snapdeal loyalists spending above ₹5,000/month on Snapdeal, Snapdeal BOBCARD offers better ROI.

- Smart cardholders with diverse needs can hold both cards simultaneously at a combined fee of just ₹748/year.

Introduction: The Online Shopping Card Dilemma

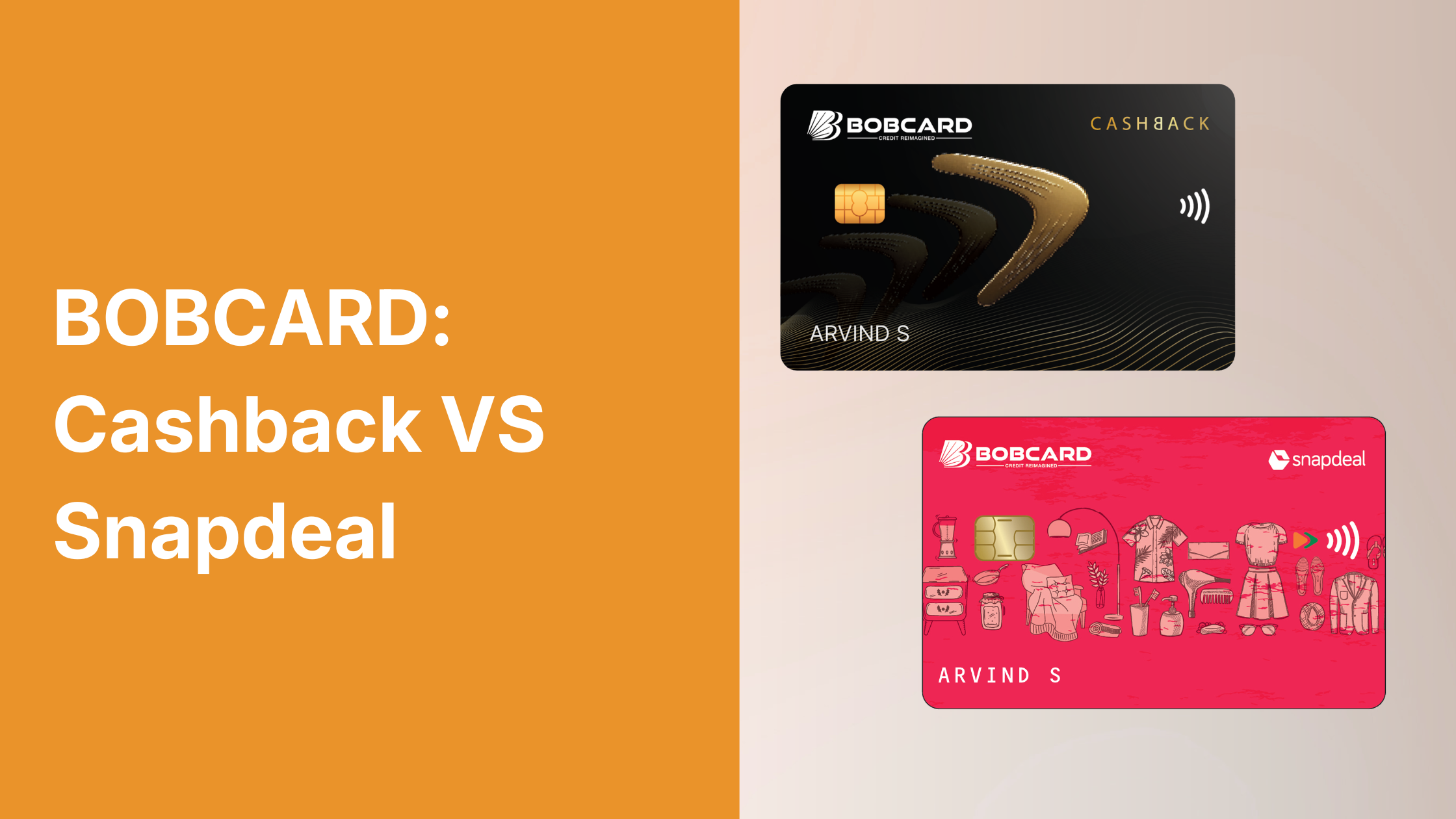

India's ecommerce boom has given rise to a new category of credit cards built exclusively for online shopping rewards. Among these, two BOBCARD products stand out for their focused cashback offerings: BOBCARD Cashback and Snapdeal BOBCARD. While both cards are designed for the same broad purpose - helping you earn more on online purchases - their strategies are fundamentally different, and choosing the wrong one for your shopping habits could mean leaving significant money on the table.

In this detailed comparison, we break down every aspect of these two cards - rewards structure, annual fees, redemption mechanics, network advantages, and realworld monthly earnings - so you can make an informed decision aligned with how you actually shop.

The Core Difference in One Sentence

BOBCARD Cashback (₹499/year) is the card for broad online shoppers who want 5% back on any eligible website, while Snapdeal BOBCARD (₹249/year) is the card for Snapdeal loyalists who want the best return specifically on Snapdeal - and a competitive 2.5% rate everywhere else.

This distinction may sound simple, but it has profound implications for your actual monthly earnings depending on where you shop most frequently. The annual fee difference of just ₹250 often becomes irrelevant when measured against the cashback differential over 12 months.

Reward Structure: HeadtoHead Comparison

| Category | BOBCARD Cashback | Snapdeal BOBCARD |

|---|---|---|

| Top cashback rate | 5% on eligible online (any platform) | 5% on Snapdeal only |

| Online shopping (nonSnapdeal) | 5% within eligible categories | 2.5% (capped ₹20K/month) |

| Departmental stores | 5% within eligible categories | 2.5% (capped ₹20K/month) |

| Groceries | 5% within eligible categories | 2.5% (capped ₹20K/month) |

| Other spends | 1% unlimited | 1% unlimited |

| Monthly cashback cap | ₹1,500 (= ₹30,000 eligible spend) | No cap on Snapdeal; ₹20K on others |

| Cashback type | Statement credit - autocredited monthly | Reward points → manual redemption |

| Annual fee | ₹499 + GST | ₹249 + GST |

| Fee waiver | No spendbased waiver | No spendbased waiver |

| Network | Mastercard | RuPay |

| UPI support | No (Mastercard) | Yes (RuPay - base rate only) |

When BOBCARD Cashback Wins

If your online shopping is spread across Amazon, Flipkart, Myntra, Meesho, Nykaa, and other ecommerce platforms, BOBCARD Cashback consistently delivers a higher effective rate. Its 5% covers a broader range of eligible categories with no platform restriction, up to ₹30,000 per month in eligible spending.

The autocredit mechanism is perhaps the card's most underrated feature. Cashback appears directly on your statement the following month - no portal login, no minimum threshold to cross, no redemption process to navigate. For the growing segment of Indian consumers who want real money back without managing reward points, this is a genuine differentiator.

The breakeven calculation is exceptionally fast: at 5% cashback, the ₹499 annual fee is recovered with just ₹9,980 in eligible online spend over the year. If you spend even ₹1,000 per month on eligible online purchases, you're in profit within the first month.

Additionally, for shoppers who frequently use categoryneutral platforms like Amazon (which carries electronics, fashion, groceries, and more), the 5% rate applies broadly without requiring you to track which category each purchase falls under.

When Snapdeal BOBCARD Wins

If Snapdeal is your primary shopping destination - fashion, electronics, home goods, personal care, kitchen appliances - the Snapdeal BOBCARD is the clear winner, and it isn't even close. The 5% cashback on Snapdeal has absolutely no monthly cap, which means your earnings scale directly with your Snapdeal spend without hitting an artificial ceiling.

Consider the numbers: a ₹10,000 Snapdeal purchase returns ₹500 in cashback. During major sale events like the Snapdeal Unbox Sale or the Big Billion Day equivalent, a ₹50,000 Snapdeal month returns ₹2,500 in cashback. There's no equivalent uncapped offering on BOBCARD Cashback, which stops earning 5% once you've accumulated ₹1,500 for the month.

The ₹249 annual fee is the lowest in the entire BOBCARD range, making the breakeven calculation even easier. Spending just ₹4,980 on Snapdeal in a year - roughly two average orders - already recovers the fee in full. Most regular Snapdeal users clear this in a single shopping session.

Beyond Snapdeal, the card's RuPay network provides a genuinely useful daily earning mechanism. Linking the Snapdeal BOBCARD to Google Pay or PhonePe allows you to earn base reward points on UPI QR code scans at local merchants - a capability that Mastercardbased BOBCARD Cashback simply cannot offer.

The 2.5% rate on nonSnapdeal online shopping, departmental stores, and grocery purchases is also competitive for a ₹249/year card. For moderate spenders outside Snapdeal, this provides a reasonable backup earning rate.

The July 2025 Snapdeal BOBCARD Change: What Cardholders Need to Know

Before July 2025, Snapdeal BOBCARD reward points were automatically credited to the card statement without any action from the cardholder - making it functionally similar to BOBCARD Cashback's zeroeffort mechanism. Since July 1, 2025, this process changed significantly.

Reward points must now be manually redeemed via the BOBCARD app or customer portal. The minimum redemption threshold is 1,000 points (equivalent to ₹250 in value). The practical implication of this change is that cardholders who do not actively monitor and redeem their points risk having them sit unspent - effectively losing the cashback value they've earned.

The recommended approach: set a recurring calendar reminder on the 1st of each month to log in to the BOBCARD app and redeem accumulated points. This takes approximately 2 minutes but ensures you capture every rupee of earned value. This change partially erodes the Snapdeal BOBCARD's previous 'zeroeffort' advantage and makes BOBCARD Cashback's automatic crediting mechanism relatively more appealing for passive earners.

Monthly Value Comparison: RealWorld Scenarios

| Monthly Scenario | BOBCARD Cashback | Snapdeal BOBCARD |

|---|---|---|

| ₹10,000 Snapdeal + ₹20,000 other online | ₹1,500 (5% on all ₹30K) | ₹500 + ₹500 = ₹1,000 |

| ₹30,000 Snapdeal only | ₹1,500 (5% on ₹30K, at cap) | ₹1,500 (5% uncapped) |

| ₹50,000 Snapdeal only | ₹1,500 (capped) | ₹2,500 (5% uncapped - clear winner) |

| ₹20,000 other online only | ₹1,000 (5%) | ₹500 (2.5%) |

| ₹10,000 Snapdeal + ₹10,000 other online | ₹1,000 (5% on both) | ₹500 + ₹250 = ₹750 |

Cashback values shown are maximum. BOBCARD Cashback requires a minimum of 4 transactions per billing cycle to qualify for the 5% rate.

Annual Fee Analysis: True Cost of Ownership

When evaluating the true cost of ownership for either card, it's important to factor in the annual fee against realistic cashback earnings over 12 months.

BOBCARD Cashback charges ₹499/year (or ₹49/month if you opt for the monthly fee plan). At 5% cashback on eligible online spends, you need just ₹9,980 in eligible annual spending to break even - roughly ₹832/month. For virtually any regular online shopper in India, this threshold is trivially easy to meet.

Snapdeal BOBCARD charges ₹249/year with no spendbased waiver. At 5% on Snapdeal, breakeven is ₹4,980 in annual Snapdeal spending - approximately ₹415/month. A single midsized Snapdeal order often exceeds this. The fee structure makes the Snapdeal BOBCARD one of the most economical cobranded credit cards in India.

Neither card offers an annual fee waiver based on spending thresholds, which means you'll pay the fee regardless of how much or how little you use the card. This is worth noting for cardholders who may use the card sporadically or during sale seasons only.

Network Comparison: Mastercard vs RuPay

The BOBCARD Cashback runs on the Mastercard network, offering excellent acceptance at online merchants, international websites, and physical POS terminals across India. However, Mastercard credit cards cannot be linked to UPI apps for QR code payments - a growing limitation as UPI captures an everlarger share of India's retail payments.

The Snapdeal BOBCARD runs on the RuPay network, which since June 2022 can be linked to UPI apps including Google Pay, PhonePe, Paytm, and BHIM. This means every QR code scan at a local kirana store, autorickshaw, restaurant, or petrol pump becomes an opportunity to earn credit card reward points - an advantage that extends the card's earning potential far beyond just Snapdeal purchases.

For shoppers who use UPI extensively for daily transactions, this RuPay advantage can add meaningful monthly earnings at the base 1% rate. UPI transactions through a linked RuPay credit card earn reward points exactly like a physical POS transaction - the points appear on your monthly statement and can be redeemed through the BOBCARD portal.

Customer Experience and Card Management

Both cards are managed through the same BOBCARD ecosystem - the BOBCARD mobile app, the customer portal at bobcard.co.in, the IVR helpline (1800 2090 / 1800 1210), and WhatsApp support at 8433 888 777.

The BOBCARD app (rated 4.1 on Google Play Store with 1M+ installs) provides realtime transaction tracking, reward point balance, statement downloads, payment options, and card controls. The app experience is consistent across both cards.

The key experiential difference remains the redemption mechanism: BOBCARD Cashback holders never need to open the app for cashback - it arrives automatically. Snapdeal BOBCARD holders must log in to redeem, which adds a minimal but recurring administrative step.

Who Should Apply for Which Card?

The decision ultimately comes down to three factors: your primary shopping platform, your monthly online spending volume, and how much you value convenience versus maximum earning potential on a single platform.

- Choose BOBCARD Cashback if you shop across multiple platforms (Amazon, Flipkart, Myntra, Meesho, etc.), want completely automatic cashback without redemption steps, and spend ₹10,000–₹30,000/month online.

- Choose Snapdeal BOBCARD if Snapdeal is your primary shopping destination, you regularly spend more than ₹20,000/month on Snapdeal (where the uncapped 5% beats Cashback's cap), or you want the lowest annual fee in the BOBCARD range.

- Consider holding both if you're a highvolume online shopper who uses both Snapdeal and other platforms heavily - the combined ₹748/year fee is offset within the first two months of regular use.

- Neither card is suitable as a primary card for travel, dining, or offline spending. Supplement with a travel or dining card for those categories.

The Verdict

For the vast majority of Indian online shoppers who spread their purchases across Amazon, Flipkart, and Myntra rather than concentrating on Snapdeal, BOBCARD Cashback is the stronger everyday card. Its autocredit mechanism, broader 5% coverage, and zeroadmin approach make it the more userfriendly option.

For dedicated Snapdeal shoppers - particularly those who spend ₹20,000+ per month on the platform - the Snapdeal BOBCARD's uncapped 5% is simply unbeatable at its price point. No other card in India offers uncapped 5% on a single platform at ₹249/year.

The smartest approach for power shoppers: hold both. The combined annual cost is less than the cashback earned on a single ₹15,000 Snapdeal purchase, making the math straightforward.

Frequently Asked Questions

Disclaimer

This article is published by Card24.ai for informational and educational purposes only. The information contained herein is based on publicly available data, product terms, and issuer communications as of May 2026, and is subject to change at any time without notice.

Card24.ai is not affiliated with BOBCARD, Bank of Baroda, or any other financial institution mentioned in this article. This content does not constitute financial advice, investment advice, or a recommendation to apply for any specific credit card or financial product.

Credit card features, annual fees, reward rates, cashback caps, and benefits are subject to change by the issuer at any time. Always verify the current terms and conditions directly with the card issuer at bobcard.co.in or by calling BOBCARD Customer Care at 1800 103 1002 before making any financial decision.

Credit card eligibility is determined by the issuing bank based on your credit score, income, existing liabilities, and other factors. Card24.ai does not guarantee approval for any card discussed on this platform.

Card24.ai may receive referral compensation from card issuers when readers apply for cards through links on our platform. This compensation does not influence our editorial content, rankings, or recommendations. All reviews are independent and based on our own research and analysis.